Q4 is most often perceived as the industry’s peak performance window. It is historically the most profitable quarter, driven by a massive influx of remaining ad spend during peak holiday user traffic. The fourth quarter of 2025 revealed a massive split: while Android Interstitials eCPMs soared by over 17% in the US, iOS Interstitials saw sharp declines across all the markets studied. Our latest report breaks down exactly why. To get a sense of the bigger picture, we recommend our previous article in the series: strong Q3 2025 performance.

Mobile apps eCPM performance Q3 2025 vs Q4 2025

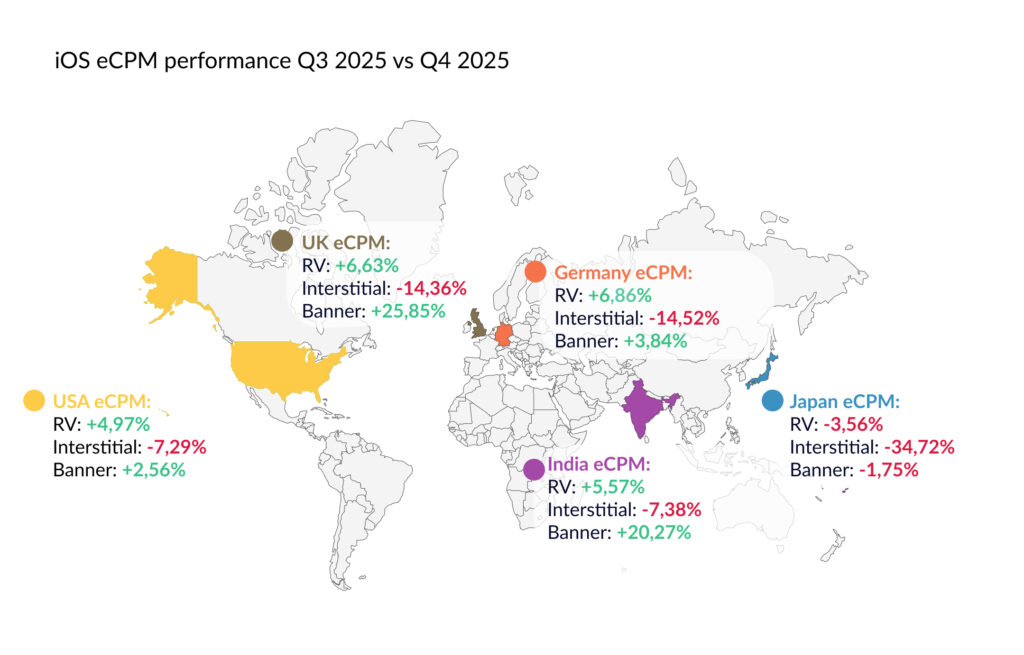

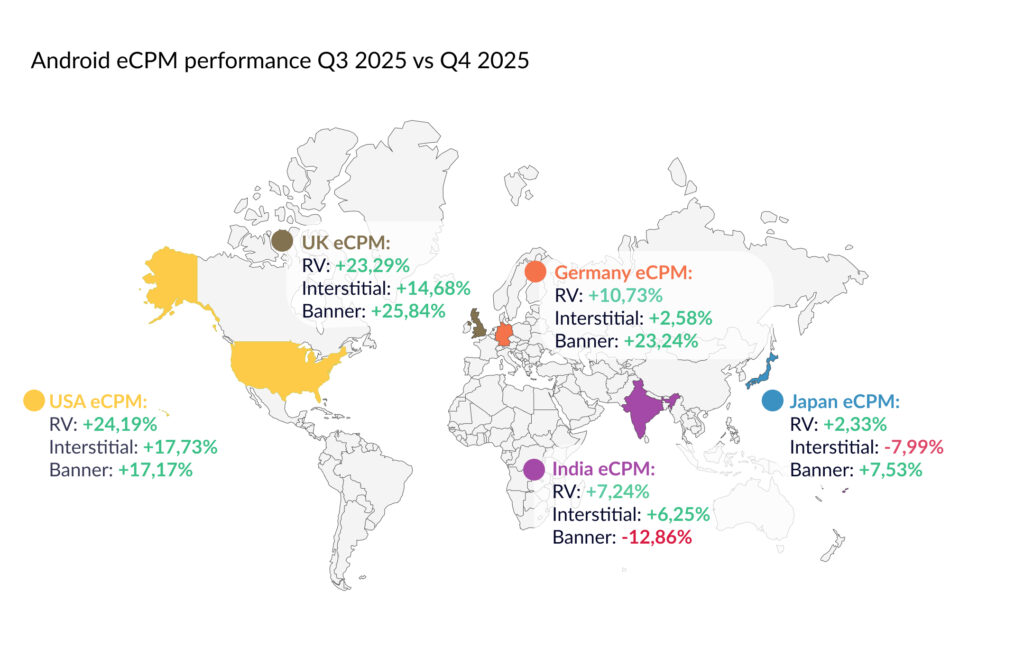

Our data maps illustrate the percentage change in eCPMs from the third to the final quarter of 2025, based on countless impressions across Bidlogic’s network. Covering both Android and iOS, we compare Rewarded Video, Interstitial, and Banner performance in the USA, UK, Germany, India, and Japan:

Interstitial ads on iOS experienced the sharpest shifts in Q4. We are seeing a significant contraction in Interstitial eCPMs across all major markets, with Japan experiencing a sharp decline of -34.72% and European markets like Germany and the UK dropping by roughly 14%. In contrast, Rewarded Video remains a bastion of stability (besides Japan, with a -3.56% decline), showing healthy growth in Germany (6.86%) and the UK (6.63%). Far from shrinking, Banners demonstrated robust health, acting as a crucial revenue stabilizer, with only a minimal decline in Japan (-1.75%).

On the Android side, the narrative is overwhelmingly positive, particularly for Rewarded Video, which is enjoying a massive efficiency spike, with no declines. The USA and UK markets are leading this charge with remarkable eCPM increases of 24.19% and 23.29%, indicating fierce competition for high-retention inventory in Tier-1 regions. Unlike their iOS counterparts, Android Interstitials are holding steady, mirroring the positive performance seen in other formats with moderate gains in Germany (6.86%) and India (5.57%). The Banner segment on Android also mirrors the high-performance trends seen on iOS, with the UK and Germany posting double-digit growth.

The volume vs. rate paradox

The decline in eCPM observed in the selected markets is driven by reduced revenue share for top-tier networks (AdMob, AppLovin, Unity, ironSource) across the selected top-5 countries, as well as lower eCPM rates across most networks, alongside an increase in the number of ad impressions. Q4 is a period of intensified advertising activity, resulting in an overall increase in the total number of ads served by all providers and contributing to greater diversification of ads across available ad networks (with a growing share of smaller providers). This has a positive impact on total revenue and the average number of ads shown per user, but not necessarily on average eCPM, as illustrated by the Interstitial format on iOS.